Bengaluru: Now in its seventh year, Ayushman Bharat, the Prime Minister’s national health insurance programme, was meant to prevent ‘catastrophic’ health expenditure that pushes 60 million Indians into poverty each year, according to union government data.

The government claims success for the Ayushman Bharat or the PMJAY (the Prime Minister’s People’s Insurance Programme), primarily with anecdotal payments of over Rs 100,000 to a few beneficiaries, as Vinod K Paul, member of the government think tank, Niti Aayog, said in October 2024.

But there is no data to support such claims of success, and studies (here, here and here) indicate the programme is not yet meeting the needs of India’s most marginalised and exposes beneficiaries to financial exploitation by private hospitals and debt.

The latest such evidence comes from a 2024 survey of low-income families in Bengaluru. It found about half of all households covered by Ayushman Bharat sought additional loans from moneylenders at usurious interest rates.

The 2025 budget for the scheme is Rs 9,406 crore, which is about 18 times lower than it should be if it were providing for the people it was meant to.

If 10% of the 600 million beneficiaries as of 2025, were to be covered, and each person made claims of Rs 50,000—the average hospital expenditure in the Bengaluru survey quoted above was about Rs 80,000—the required budget would be Rs 300,000 crore, of which the centre should contribute 60% or Rs 180,000 crore.

Since Ayushman Bharat was launched in September 2018, according to data for the period 2018-23, collected from the PMJAY dashboard, the latest available, the number of beneficiaries receiving payments of over Rs 100,000 was just 1.1% or 328,000.

With these 600 million beneficiaries, Ayushman Bharat has successfully created a demand for health insurance. But the supply of hospital beds in empanelled or authorised hospitals has not matched the demand: less than half of the estimated 70,000 hospitals nationwide are empanelled to support the PMJAY scheme.

The government reported 825,000 hospital beds in an estimated 70,000 hospitals in India based on a National Health Profile report in 2021. A January 2024 government report quoted 1.33 million hospital beds in about 28,000 empanelled hospitals or less than half the total number of hospitals in India.

If the data from the 2021 report are assumed to be accurate, then the number of beds in empanelled hospitals would be about 400,000. With 600 million beneficiaries, this would represent about 0.75 hospital beds per thousand which is close to reported figures, but far below the recommended two beds per 1,000.

India’s Health Problem

The Indian government spends 1.35% of its gross domestic product (GDP) on healthcare, among the lowest in the world, while low- and middle-income countries spend around 6% GDP on public healthcare.

So, it isn’t surprising that Indians spent more money on private healthcare than most others worldwide.

Modi’s government launched the Ayushman Bharat scheme to achieve its vision of universal health coverage. There were two complimentary components: cashless health insurance coverage up to Rs 500,000 for the poor at public and private hospitals; and 150,000 health and wellness Centres to deliver primary care.

With out-of-pocket (OOP) expenditure down from 69% of current health expenditure in 2013 to 39% in 2021—according to the latest data (pg 35) made available in December 2024—the government has claimed that Ayushman Bharat has been largely successful and “saved crores of families” from catastrophic expenditure.

The programme does not cover outpatient costs, which include medicines that make up two thirds of health expenditure, as Article 14 reported in August 2023 in an investigation from the Prime Minister’s home state, Gujarat.

Experts had then said that the PMJAY website showed “selective data”, and there was “no transparency or independent evaluations”, making a verdict on the programme’s success in reducing out-of-pocket expenses difficult.

Unless the government invested in public health care, regulated private healthcare and enabled affordable medicines, experts argued, the PMJAY would not help the majority of the people it was meant to and stem the plunge into poverty it was meant to prevent.

New Survey Confirms Old Problems

In April 2024, the Azim Premji Foundation, a nonprofit, sponsored a health survey of over 1,000 low income families in 12 different areas of South Bangalore. Over 4,000 individuals responded to the roughly 50 questions.

The survey was divided into two parts. One part was questions that pertained to a household and the other part was about the individuals in a household.

About 20% of the households had some health insurance coverage through either an employer or the government. Over 12% of households had used the Arogya Karnataka Health Scheme, a state scheme integrated with PMJAY in October 2018, to cover their medical expenditure.

About 40% of all households reported an average hospitalisation expenditure of Rs 79,000 in 2023-24. From claim data collected from the PMJAY dashboard during 2018-23, the average beneficiary received less than Rs 10,000 from an empanelled hospital.

The balance of almost Rs 70,000 is the out-of-pocket expenditure that a household must bear.

The High Cost of Borrowing

About 75% of the 40% households who reported some hospitalisation expense, borrowed money. Half of the 322 households in the survey who borrowed funds for hospitalization expenses used moneylenders. The remaining major sources for funds included gold loans and family. The period for the interest charged varied from weekly, monthly, to annually.

93% of moneylenders charged an average interest rate of 6% per month or 72% annually. The 26% of the 322 households who used gold loans paid an average interest rate of 4.5% per month or 54% per year. While some of the 10% of households who borrowed from families received loans at 0% interest, the average interest rate was 7.5% per month or 90% per year.

Although the Karnataka Prohibition of Charging Exorbitant Interest Act, 2004, caps the interest rate for loans at 18% per year (or 1.5% per month), moneylenders continue to charge significantly higher interest rates.

With a large number of such households falling into a debt trap, no one can dispute the need for a health scheme like PMJAY. But the scheme is seriously underfunded to justify the claim of the world’s largest health scheme.

Promise & Limitations Of Predecessor

The idea of providing universal health coverage in 2018 was not novel and the Ayushman Bharat scheme was preceded by the Rashtriya Swasthya Bima Yojana (RSBY) or the national health insurance programme and the Senior Citizen’s Health Insurance Scheme.

Ayushman Bharat was meant to replace the RSBY, which had not achieved its primary goal (here and here) of reducing out-of-pocket expenses incurred by lower-income families.

High out-of-pocket expenses can force a low income family into financial hardship that may include falling back into poverty, borrowing from money lenders at exploitative interest rates up to 60%, or forgoing basic needs, such as food, affordable housing and education.

Over an eight-year period from 2008 to 2016, over 150 million people enrolled in the RSBY. The results on out-of-pocket expenditure were mixed.

One of the RSBY’s limitations was that it was limited to inpatient treatment and hospitalisations alone. In general, hospitalisation costs are significantly higher than outpatient costs and it seemed logical to first cover the most expensive share of healthcare expenses.

A study based on survey data collected in 2010-11 showed that the out-of-pocket expenditure of beneficiaries had actually increased by 30% despite RSBY.

One explanation for this unexpected outcome was that beneficiaries were more willing to seek treatment for short term illnesses even though the payments would be borne by the patient. This additional expense led to a higher out-of-pocket expense.

Further RSBY Problems

With the security of being covered in case a short term illness becomes a hospitalisation, a larger number of patients sought primary health care. The higher cost of out-of-pocket expenses were compensated for by a decrease in the number of sick days.

On the other hand, a government study showed that out-of-pocket expenses actually declined from 62% in 2014 to 49% in 2018, a four-year period prior to the introduction of Ayushman Bharat, when the RSBY scheme was being implemented. The decline was due to the increase in government health expenditure, according to the National Health Accounts data 2020-21 (pg 41).

The annual premium for the RSBY scheme was Rs 750 with the union government covering 75% or Rs 565 and the state covering the balance of Rs. 185 for coverage of Rs 30,000.

In 2017-18, the cost of the scheme for about 35 million families at a premium of Rs. 750 per family was Rs 2,625 crore. However, the government reported just Rs 456 crore had been used in 2018.

The RSBY scheme attracted worldwide attention despite an actual expenditure of just 0.1% of the 2018 budget. About 10% of India’s population had enrolled in the RSBY scheme, even with the low coverage of Rs 30,000.

RSBY’s success in providing some coverage to about 140 million people set the stage for the introduction of a more ambitious health scheme.

The Ayushman Bharat Revamp

Due to inflation, the value of the Rs 30,000 coverage that the RSBY provided in 2008 had roughly halved 10 years later. By 2018, the cost of a few days of hospitalisation in an intensive-care unit could easily exceed Rs 30,000.

In September 2018, Prime Minister Modi announced the Pradhan Mantri Jan Arogya Yojana (PMJAY) scheme, a national health protection scheme to replace the RSBY scheme. The PMJAY scheme was part of the wider Ayushman Bharat health reform. In addition to the protection from hospitalization costs that was earlier covered under the RSBY scheme, Ayushman Bharat also included the creation of 150,000 health and wellness centres.

The purpose of the health and wellness centres was to provide primary health care that was lacking in the RSBY scheme. The PMJAY Scheme also increased coverage by over 16 times to Rs 500,000. However, due to inflation the coverage of Rs 500,000 in 2018 was worth Rs. 375,000 in 2025.

A private insurer reported a higher medical annual inflation rate of 14%, which would reduce the value of the coverage of Rs 500,000 in 2018 to just Rs. 200,000 in 2025.

In addition to the higher coverage under PMJAY, the number of beneficiaries was increased from about 150 million (under RSBY) to about 500 million. While a 16-fold increase in PMJAY coverage and a three-fold increase in the number of beneficiaries was welcome, the budget for the scheme was not increased in proportion to the increase in number of beneficiaries and higher coverage.

The initial budget in 2018 for the Ayushman Bharat was Rs 2 ,400 crore, of which about 75% was utilised. By 2025, the budget was increased to Rs 9,600 crore.

In response to questions in Parliament, details of the PMJAY scheme (as of February 2024), including funds allocated/utilised, insurance collected by hospitals, and number of beneficiaries, was published online.

About 90% of the budget was utilised between 2018-24: 15.4 million claims were made in 2022-23, and 14.7 million claims settled. With an expenditure of Rs 6,000 crore in 2022-23, the average payment per claim was about Rs 4,100. In January 2025, Rs 3,920 crore out of the allocated Rs 4,100 crore was utilized.

The PMJAY Dashboard

Detailed statistics about the PMJAY scheme are published on a government website. The statistics include the total number of Ayushman Bharat cards created, number of authorised hospital admissions, and the number of empanelled hospitals.

An empanelled hospital is a part of a network of hospitals that have been chosen based on some quality standards set by the government, where a beneficiary can seek cashless treatment.

The trends in these statistics over a year are also available.

The bottom of the webpage gives detailed claim information for every empanelled hospital in every district and every state. For example, the Government General Hospital in Kasargod, Kerala, reported 10,000 beneficiaries since 2019. The spreadsheet for the hospital includes the name of the patient, the date and payment. A spreadsheet is published for each of the 25,643 empanelled hospitals organised by state and district.

Statistics generated from the collection of spreadsheets are based on data at a higher granularity than the statistics published at the top of the website. Over 99% of the hospitals in the spreadsheet data did not report any data for 2024.

While the webpage reports over 31,000 empanelled hospitals nationwide, the spreadsheet data includes 25,643 such hospitals.

Though the spreadsheet data does not correspond with the summary data on the same webpage, it is still useful to draw some general observations about the implementation of the PMJAY scheme between 2018 and 2023 using the spreadsheet data.

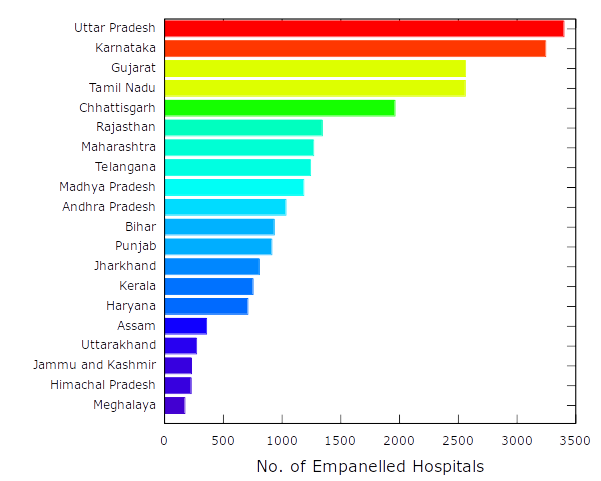

The number of empanelled hospitals per state ranged from several thousands to a handful. The top 20 states with the highest number of such hospitals include the most populous states. The population per empanelled hospital varied from state to state.

The number for some states, such as Gujarat and Tamil Nadu, was between 20,000 to 30,000, while states such as Bihar, Maharashtra and Assam had over three times as many people per empanelled hospital.

The number of empanelled hospitals nationwide varied from 1-25 for over 50% of all districts to over 100 for 5% of all districts. In most cases, districts with higher populations tended to have a higher number of empanelled hospitals.

However, exceptions include the district of Vijayapura in Karnataka with 2,722 hospitals and the district of Banaskantha in Gujarat with 267 hospitals.

Locating Hospitals & Other Challenges

Even with the availability of empanelled hospitals in a beneficiary’s district, locating the nearest hospital that will accept the PMJAY insurance scheme is a challenge. The government does provide a webpage to search for hospitals.

In any case, it is not convenient to find the closest hospital near a beneficiary. An Android app called Ayushman does provide a search for hospitals by pincode, district, and name of the hospital. Each hospital is geo-tagged and includes the list of specialities.

In the Azim Premji Foundation survey described above, one of the main reasons cited by beneficiaries for not visiting a health centre was the distance. The location of hospitals that accept PMJAY insurance is known and given a beneficiary’s location, it should be possible to find the nearest five or six hospitals.

Finding a hospital that accepts PMJAY insurance is also not a guarantee of treatment. For instance, in December 2024, a 72-year-old Bengaluru resident committed suicide after learning that he was not eligible for cancer treatment under PMJAY at the Kidwai Memorial Institute of Oncology, even though the Institute had covered several hundred other beneficiaries with an average payout of about Rs 8,300.

In September 2024, the PMJAY scheme was expanded to include all individuals above 70, regardless of income. That meant the 72 year old was eligible for PMJAY, for which he had enrolled.

In another similar case, an 87 year old was told by a private hospital that the PMJAY card could not be accepted as instructions had not been received from the state government. The ruling Karnataka Congress government and the central BJP government traded accusations and blame.

Tussles Between Centre & State

In January 2025, Bengaluru Bharatiya Janata Party member of Parliament Tejasvi Surya claimed that the union government was committed to paying 60% of the costs for PMJAY, while the state government must bear the remaining 40%. In response, the state government claimed that it was bearing 75% of the costs and not 40%.

It appeared that Ayushman Bharat beneficiaries are often caught up in the tussle for funds between union and state governments.

Despite the differences between the union and state governments, the southern states have dominated the number of hospital admissions. The Ayushman Bharat spreadsheet data in the period 2018-23, shows that Karnataka, Kerala, and Tamil Nadu had 4.8, 3.8, and 3.7 million hospital admissions respectively.

In the spreadsheet data , not every hospital admission resulted in a payment. Out of the total 30 million admissions from 2018 till 2023, about 21.4 million or 71% received some payment. No payment was listed for the remaining 8.6 million beneficiaries.

The order of the number of hospital admissions by state did not correspond with the order of the total payments for a state. The top three states by payments were Andhra Pradesh (Rs 400 crore), Maharashtra (Rs 365 crore), and Tamil Nadu (Rs 331 crore).

Of the top five districts by payment, four were in south India. Karnataka’s Vijayapura district with payments of Rs 143 crore was followed by Chennai (Rs 60 crore), Guntur in Andhra Pradesh (Rs 55 crore), Visakhapatnam in Andhra Pradesh (Rs 54 crore), and Ahmedabad in Gujarat (Rs 50 crore).

Despite a formula for sharing healthcare costs between the union and state government in a 60:40 ratio, the states paid for a majority of the health costs.

The Centre reported rising government health expenditure in 2020-22 with states bearing about 64% of all costs and the centre the remaining 36%.

Data Discrepancies

The maximum payment to a beneficiary exceeded Rs 500,000 in about 100 of 25,643 hospitals registered with Ayushman Bharat. Ten hospitals in Andhra Pradesh and Telangana reported a maximum payment of over Rs 10 lakh. The average of the highest payment of all 25,643 hospitals was about Rs 43,000.

The total payments by all hospitals for the period 2018-23 in the spreadsheet data was about Rs 26,000 crore. Out of 25,643 hospitals, about 5000 reported zero payments while about 4500 reported payments of over Rs 1 crore. Four hospitals reported payments of over Rs 100 crore with the maximum of Rs. 143 crore for 36,000 beneficiaries at SJICR Hospital, Vijayapura, Karnataka.

In January 2025, the government reported payments of over Rs 100,000 crore or about four times the amount in the spreadsheet data. The explanation for the higher estimate of over Rs. 100,000 crore was that if beneficiaries were to seek treatment outside of the PMJAY network, they would have paid about double the amount that was covered by insurance.

Another explanation for the savings of over Rs 100,000 crore in out-of-pocket expenses was the greater focus on primary health care.

The need for secondary and tertiary care decreased as a result of higher primary health care expenditure. In the spreadsheet data, the number of primary and secondary health care centers were about 5,500 and 3,000 respectively. The number of primary and secondary health care centers in government data was significantly higher at 30,000 and 6,000 respectively.

The estimated total budget between 2018 to 2025 (pg 28) for PMJAY was about Rs 32,500 crore. In most years during the seven-year period, the entire budget was not used. As of December 2024, hospital admissions worth about Rs 116,000 crore were authorised under the PMJAY scheme. The shortfall of about Rs 83,500 crore would have to be covered by the state or by the beneficiary.

Further Problems

In 2024, the government reported savings of Rs 125,000 crore in out-of-pocket expenses, roughly five times the total budget for PMJAY of about Rs 25,000 crore from 2018-24.

Claims of PMJAY beneficiaries from 2018-23 were settled at an average payout of Rs 4000 per claim. The multiplier effect of five times would increase the actual value of the payout per claim to Rs 20,000. The savings in out-of-pocket expenses have ripple effects, including:

- Lower healthcare expenses: the need for borrowing or depleting savings is reduced, increasing financial stability of a household. Borrowing from moneylenders at a high interest rate to pay for healthcare expenses is often a debt trap from which low income families cannot escape

- Higher savings: money saved from healthcare expenditure is used on goods and services, education, and housing

- Higher productivity: households are likely to be more productive with fewer hospitalisations. This is possible with preventive primary health care

However, accurately quantifying the multiplier effect to evaluate the economic benefits for every rupee spent on the PMJAY health scheme is not obvious.

The formula for calculating the multiplier effect depends on the increase in spending due to the payments from Ayushman Bharat.

Economists do not commonly use the multiplier effect (pg 2) to measure the effectiveness of additional government spending. This is because of the difficulty in isolating any particular government spending as the sole cause for any improvement in the economy.

The other major issue with PMJAY is the delayed reimbursement to private hospitals. Delays in reimbursement discourage private hospitals from joining the list of empanelled hospitals.

This limits the number of hospitals where a beneficiary can seek treatment, which can lead to overcrowding at fewer empanelled hospitals. Further, the government rates for various treatments are in general lower than the costs that hospitals claim.

The government’s response to Parliament in December 2024 to the issue of delayed payments to private hospitals has been uninformative. The response did not provide any specifics on the percentage of delayed payments or the amounts that are due to private hospitals.

The PMJAY dashboard does provide information about claims for the Central Government Health Scheme (CGHS) but not directly for the PMJAY scheme. The payments made by empanelled hospitals under PMJAY are described in individual spreadsheets and are often not updated.

In a 2021 survey of 31 empanelled hospitals (eight public and 23 private) in Uttar Pradesh, the PMJAY was viewed poorly in comparison to private health insurance by over 77% of the participants. The three main reasons for the poor review of the PMJAY were denial of reimbursement, delays in processing of claims, and a lack of grievance redressal.

While most private hospitals were reluctant to become empanelled PMJAY hospitals for these reasons, the number of PMJAY cards issued in January 2025 exceeded 360 million. A single card can be used by all members of a family.

The promise of paid health care under Ayushman Bharat does not match increasing demand—or its claims.

The Proliferation of ID Cards

The Ayushman Bharat Digital Mission (ABDM) was created to provide the digital infrastructure to support the implementation of the Ayushman Bharat scheme.

The mission of ABDM was to maintain consistency of medical records for every participant that could be accessed by registered health care facilities from primary clinics to specialised hospitals.

In February 2025, the government claimed that almost half of India’s population had created Ayushman Bharat Health Account (ABHA) cards. Each ABHA card was associated with an unique 14 digit (ABHA) number and linked to an Aadhar card.

The ABHA card is distinct from the PMJAY card in that the ABHA card is used to manage an individual’s health records alone and does not provide any insurance coverage.

While there is no question that a medical professional will be able to prescribe better treatment given access to the current medical records of a patient, the problems in the implementation of ABHA are difficult to solve.

The first problem is ensuring the privacy of health records. After making it compulsory for the roughly 4.5 million central government employees covered under the CGHS scheme to link their CGHS card with the ABHA card, the government changed its mind over potential issues with privacy.

The second problem is the lack of interoperability between software systems. Many healthcare providers use proprietary software and there is currently no standard for medical records across all clinics, hospitals, and health centers. Migrating from one software system to a common system is an expense that can be prohibitive for private healthcare providers.

Storing scanned images of paper documents is not sufficient for a truly digital system. Extracting, collating, and summarising data from PDF files or images is complex and likely to have errors. Further, the handwriting of some medical staff is not always legible.

Finally, the success of the ABHA system depends on individuals and healthcare providers updating and maintaining health records online. Without the disciplined and active participation of both to keep the ABHA information current, doctors will fall back to the old system of papers in a folder.

(Manu Konchady is an author specializing in data analysis and software development.)

Get exclusive access to new databases, expert analyses, weekly newsletters, book excerpts and new ideas on democracy, law and society in India. Subscribe to Article 14.